{beginAccordion h2}

Six Most Overlooked Tax Deductions

By: Servion Financial Preferred Investments & Insurance

Who among us wants to pay the IRS more taxes than we have to?1

While few may raise their hands, Americans regularly overpay because they fail to take tax deductions for which they are eligible. Let’s take a quick look at the six most overlooked opportunities to manage your tax bill.

- Reinvested Dividends: When your mutual fund pays you a dividend or capital gains distribution, that income is a taxable event (unless the fund is held in a tax-deferred account, like an IRA). If you’re like most fund owners, you reinvest these payments in additional shares of the fund. The tax trap lurks when you sell your mutual fund. If you fail to add the reinvested amounts back into the investment’s cost basis, it can result in double taxation of those dividends.2 Mutual funds are sold only by prospectus. Please consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

- Job Hunting Costs: A tough job market may mean you are looking far and wide for employment. The costs of that search—transportation, food and lodging for overnight stays, cab fares, personal car use, and even printing resumes—may be considered tax-deductible expenses, provided the search is not for your first job.

- Out-of-Pocket Charity: It’s not just cash donations that are deductible. If you donate goods or use your personal car for charitable work, these are potential tax deductions. Just be sure to get a receipt for any amount over $250.

- State Taxes: Did you owe state taxes when you filed your previous year’s tax returns? If you did, don’t forget to include this payment as a tax deduction on your current year’s tax return.

- Medicare Premiums: If you are self-employed (and not covered by an employer plan or your spouse’s plan), you may be eligible to deduct premiums paid for Medicare Parts B and D, Medigap insurance, and Medicare Advantage Plan. This deduction is available regardless of whether you itemize deductions or not.

- Income in Respect of a Decedent: If you’ve inherited an IRA or pension, you may be able to deduct any estate tax paid by the IRA owner from the taxes due on the withdrawals you take from the inherited account.3

1The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

2Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

3Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2017 FMG Suite.

Your Emergency Fund: How Much Is Enough?

By: Servion Financial Preferred Investments & Insurance

Have you ever had one of those months? The water heater stops heating, the dishwasher stops washing and your family ends up on a first-name basis with the nurse at urgent care. Then, as you’re driving to work, giving yourself your best, “You can make it!” pep talk, you see smoke seeping out from under your hood.

Bad things happen to the best of us, and instead of conveniently spacing themselves out, they almost always come in waves. The important thing is to have a financial life preserver, in the form of an emergency cash fund, at the ready.

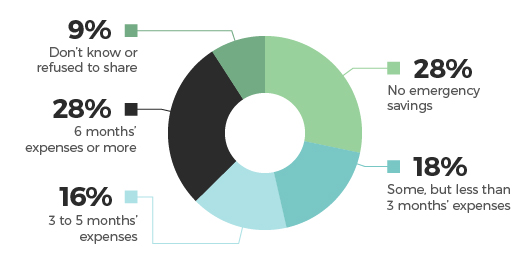

Although many people agree that an emergency fund is an important resource, they’re not sure how much to save or where to keep the money. Others wonder how they can find any extra cash to sock away. One survey found that 28% of Americans don’t have any emergency savings at all.1

How Much Money?

When starting an emergency fund, you’ll want to set a target amount. But how much is enough? Unfortunately, there is no “one-size-fits-all” answer. The ideal amount for your emergency fund may depend on your financial situation and lifestyle. For example, if you own your home or provide for a number of dependents, you may be more likely to face financial emergencies. And if the crisis you face is a job loss or injury that affects your income, you may need to depend on your emergency fund for an extended period of time.

Coming Up with Cash

Fast Fact: Only 10% of people with a college degree say they have no emergency savings, compared to 42% of those with a high-school education or less. – Bankrate.com, June 21, 2016

If saving several months of income seems an unreasonable goal, don’t despair. Start with a more modest target, such as saving $1,000. Build your savings at regular intervals, a bit at a time. It may help to treat the transaction like a bill you pay each month. Consider setting up an automatic monthly transfer to make self-discipline a matter of course. You may want to consider paying off any credit card debt before you begin saving.

Once you see your savings begin to build, you may be tempted to use the account for something other than an emergency. Try to budget and prepare separately for bigger expenses you know are coming. Keep your emergency money separate from your checking account so that it’s harder to dip into.

Where Do I Put It?

An emergency fund should be easily accessible, which is why many people choose traditional bank savings accounts. Savings accounts typically offer modest rates of return. Certificates of Deposit may provide slightly higher returns than savings accounts, but your money will be locked away until the CD matures, which could be several months to several years.

The Federal Deposit Insurance Corporation insures bank accounts and certificates of deposit (CDs) up to $250,000 per depositor, per institution in principal and interest. CDs are time deposits offered by banks, thrift institutions, and credit unions. CDs offer a slightly higher return than a traditional bank savings account, but they also may require a higher amount of deposit. If you sell before the CD reaches maturity, you may be subject to penalties.

Some individuals turn to money market accounts for their emergency savings. Money market funds are considered low-risk securities, but they’re not backed by any government institution so it is possible to lose money. Depending on your particular goals and the amount you have saved, some combination of lower-risk investments may be your best choice.

Money held in money market funds is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Money market funds seek to preserve the value of your investment at $1.00 a share. However, it is possible to lose money by investing in a money market fund. Money market mutual funds are sold by prospectus. Please consider the charges, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

The only thing you can know about unexpected expenses is that they’re coming — for everyone. But having an emergency fund may help alleviate the stress and worry associated with a financial crisis. If your emergency savings are not where they should be, consider taking steps today to create a cushion for the future.

Where Do You Fit In?

Here’s a look at how Americans are doing when it comes to emergency savings:

1Bankrate.com, June 21, 2016

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2017 FMG Suite.

What to Look for in Personal Finance Apps

By: Servion Financial Preferred Investments & Insurance

Since Apple launched its iPhone App Store in July 2008, the mobile applications market has exploded.

In 2016, Statista reported that Apple customers had downloaded 130 billion apps. On the other side of the smart phone universe, Android users have downloaded 65 billion apps since the Google Play launch in 2010.1

To put those numbers in perspective, that’s over 26 apps downloaded for every person on the planet.2

While many of these apps are games and social media programs, an increasing number have been developed to help individuals with their personal finances. Which leads to an interesting question: what should you look for in a personal finance app?

Tip: Like any good tool, apps are as useful as you make them. An app may be able to help with financial decisions and transactions, but it won’t get you to stick to a budget.

Category

One of the first things to consider is what type of financial apps may be most useful. Bankrate.com breaks them into four categories:

Budget tracking apps allow users to record expenditures as they are made to keep track of bank balances and budget categories. Some allow users to make a budget and then watch how closely expenditures are tracking to it.

Financial assistant apps collect, store, and report information from users’ various savings and investment accounts, providing a single place to keep track of asset performance.

Loan calculator apps estimate payments and current balances for loans. Some also track how long it will take to pay off one or more loans.

Spending and saving apps allow users to perform a wide-range of activities, including “what if” scenarios.

Fast Fact: By 2020, nearly 40% of the world's population will own a smartphone. That amounts to almost 2.9 billion users worldwide. Source: Statista.com, 2017

Criteria

Once a user has decided on a category of app that may be useful, there are additional criteria to consider.

Credibility. As everyone knows, not everything written on the internet is true. For example, The Wall Street Journal and The New York Times are generally considered more credible than an anonymous blog. The same principle applies to apps: understand who’s providing the information.

Security. Before using any financial app, read the privacy or security statement. This can typically be found at the bottom of the company's web page or in the About section of their website. If you don't find one online, contact the company to request a copy.

Clarity. A personal finance app should provide information that is easy to understand. There are some apps that provide detailed charts on stock performance using a wide variety of financial analyses. However, if you don’t understand the underlying analysis, the app may be useless.

Relevance. Remember the old saying: “If the only tool you have is a hammer, you tend to see every problem as a nail.”3 The same applies to financial information. A mutual fund company may be a great source of information about mutual funds, but it may be less useful at providing information about estate planning.

Using an app to help with your personal finances may be a great first step in becoming a better money manager. And asking yourself a few key questions before you download may help you select the app that best fits your personal finance needs.

1Statista, 2016

2U.S. Census Bureau, 2016

3Abraham Maslow quote from Brainy Quote, 2016

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2017 FMG Suite.

{endAccordion}